Debt Sustainability

- Edward Ballsdon

- Dec 17, 2025

- 7 min read

Updated: Mar 6

INTRODUCTION This note examines the growing macroeconomic and political risks associated with elevated government debt. It draws on three decades of analysis of the Japanese economy, the Japanese Government Bond (JGB) market, and the policy frameworks implemented by both the government and the Bank of Japan.

Debt sustainability - like currency debasement - is a critical but often poorly understood topic. Over the past 20 years, most advanced economies have substantially increased their borrowing, first in response to the Global Financial Crisis and later during the COVID‑19 pandemic. The resulting expansion in public debt now acts as a structural drag on future economic growth. Moreover, the policies that will eventually be required to address these debt burdens carry a significant risk of triggering future financial instability.

This article focuses on the deterioration in Japan’s debt sustainability. A subsequent piece will examine the policy responses that are likely to emerge and their implications for the broader Japanese economy. The analysis draws on research and commentary provided to clients over the past two years, which have consistently highlighted the emergence of this issue.

WHAT IS "DEBT SUSTAINABILITY"?

Spain required assistance from the European Central Bank in 2012 when its government debt stood at only 70% of GDP, whereas Japan—whose Debt‑to‑GDP ratio was 185% at the time—was entirely unaffected by the European sovereign debt crisis. Why was Spain in distress while Japan remained stable despite having far higher indebtedness?

The key point is that commonly cited ratios such as Government Debt/GDP and Annual Interest Costs/GDP reveal very little about a sovereign’s true ability to service its obligations. This is similar to corporate analysis: no one would judge a company’s solvency using Debt/Sales or Interest Costs/Sales, as these metrics ignore the firm’s capacity to generate the cash flow required to service debt. Consider that

If a company is profitable, the operating cash flow it generates is sufficient to cover interest expenses and reduce outstanding debt.

If it is loss‑making, it must borrow to meet interest payments and refinance maturing obligations with new debt.

For corporate borrowers, the Interest Costs / Operating Cash Flow ratio is therefore a meaningful measure of debt‑servicing capacity, alongside several other useful financial indicators.

Because most governments run persistent fiscal deficits - where tax revenues fall short of expenditures - they resemble loss‑making companies (*1). Their equivalent of a corporate interest‑cost‑to‑operating‑cash‑flow ratio is always negative, because the “operating cash flow” (the net budget position) is negative by definition. This is one reason analysts turn to alternative metrics of debt sustainability, including the commonly cited but often uninformative Debt‑to‑GDP ratio.

A more meaningful indicator of debt sustainability focuses on whether annual interest costs remain manageable within the government’s overall budget. The key metric is the annual Interest Cost / annual Government Revenue (IC/GR) ratio, which signals when interest payments begin absorbing too large a share of fiscal resources and start constraining a government’s policy agenda.

In Japan’s case, this ratio is now rising sharply, indicating growing stress in the JGB market. If current trends persist, 2026 could mark the point at which a disorderly adjustment in JGB prices triggers heightened volatility across Japanese financial assets and the yen.

SETTING THE SCENE

I have followed Japan closely since the collapse of the Nikkei and Japanese real‑estate bubbles in 1990. Over this period, three distinct phases have emerged:

1. The “Lost Generation” (1990–2011)

The private sector deleveraged, while the government ran large fiscal deficits, driving the Debt‑to‑GDP ratio from 45% to 170%.

The yen remained stable, JGBs appreciated as yields fell toward 0%, and equity and real‑estate prices declined sharply until around 2010.

2. Abenomics (2011–2024)

Private‑sector leverage remained flat, but persistent government deficits pushed Debt‑to‑GDP to roughly 225%.

The BoJ expanded its balance sheet significantly; by 2024 it owned around 50% of all outstanding JGBs through Quantitative Easing (QE) and Yield Curve Control (YCC).

The yen began to depreciate, JGB valuations remained stable, and equity and real‑estate markets recovered.

3. The “BoJ Death Wish” (2024– )

Private‑sector leverage remains stagnant and fiscal deficits continue.

The BoJ abandoned YCC and reduced net JGB purchases, effectively initiating a phase of stealth Quantitative Tightening (QT).

JGB yields have risen, the yen has continued to weaken, and equities ultimately recovered in 2025 following a flat 2024.

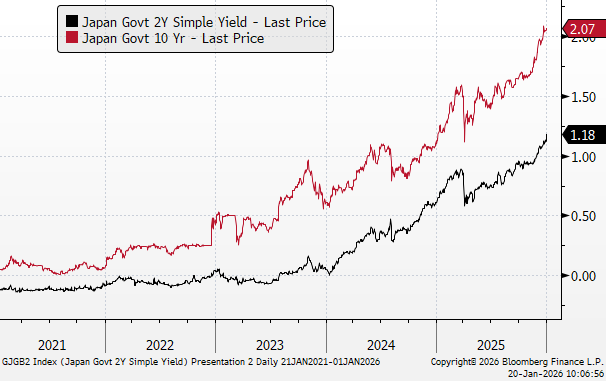

Throughout the Lost Generation and Abenomics periods, the Bank of Japan pursued aggressive monetary easing, repeatedly cutting policy rates and ultimately implementing a Zero Interest Rate Policy (ZIRP). This sustained decline in interest rates pushed JGB yields steadily lower even as the stock of government debt expanded sharply. As a result, the government’s total annual interest burden remained contained: the weighted average interest rate on outstanding JGBs fell from 6.10% in 1990, when total debt stood at ¥320 trillion, to just 0.77% in 2023, even though outstanding debt had risen to ¥1,230 trillion.

This stabilising dynamic began to reverse when the BoJ started raising rates.

THE BOJ’S “DEATH WISH”

A death wish is a psychoanalytic term referring to a conscious or unconscious desire for self‑destruction. The phrase is an apt metaphor for the Bank of Japan’s policy stance since 2024. The BoJ has tightened policy on two fronts:

by raising interest rates, and

by purchasing fewer JGBs under its QE programme than the volume of bonds maturing on its balance sheet.

This combination has reduced the BoJ’s share of the JGB market and effectively initiated a form of stealth quantitative tightening. The Bank has justified these actions on inflation grounds, despite underlying price pressures remaining subdued. Traditional Core CPI (excluding food and energy) has held in a narrow 1.3% - 1.6% range since July 2024, and all four core sub‑indices (Choice, Burden, Services, and Goods) have remained below the BoJ’s 2% target.

As a direct consequence, nominal JGB yields have moved higher.

The rise in JGB yields has a direct and ongoing fiscal consequence: the government must now issue new debt at significantly higher interest rates than in the past. This affects both:

New issuance required to finance the annual fiscal deficit, and

Refinancing issuance, where low‑coupon maturing bonds are replaced with higher‑yielding debt.

The most recent budget projected annual interest costs of ¥10,523 billion for the current fiscal year, a figure that already appears understated given the sharp increase in yields. Looking ahead, it is possible to estimate how interest expenditures will evolve under current conditions. If:

market‑implied forward yields materialise, and

the fiscal deficit remains unchanged,

then annual interest costs would rise to ¥23,850 billion by 2030, an increase of 127%. This outcome reflects a rise in the weighted average interest rate on outstanding government debt from 1.1% today to 1.9% by 2030.

Moreover, if future JGB yields end up 25bp, 50bp, or 100bp above current market pricing, the fiscal impact becomes even more severe. Scenarios A, B, and C in the accompanying chart illustrate how rapidly annual interest costs could escalate—even though the weighted average interest rate would still remain modest by historical standards.

Returning to the question of debt sustainability, the most important metric is annual interest costs as a share of government budget revenues (the IC/TR ratio), which are primarily composed of tax receipts. For this analysis, I assume tax revenues continue growing at their recent trend rate of 4.5% per year.

The chart below shows that the IC/TR ratio bottomed in 2023 and has since risen sharply. These dynamics - both the earlier decline from 2011 and the subsequent reversal - closely mirror shifts in BoJ policy. The implication is clear: if market‑implied forward rates materialise, annual interest costs would absorb 22% of all tax revenues by 2030, placing substantial pressure on the fiscal framework.

The chart above illustrates why the BoJ’s current policy stance amounts to a death wish. These outcomes are the direct result of its own policy choices, and the fiscal damage will be significant—even under relatively benign assumptions.

The Base Case scenario is already severe. It simply reflects current market expectations for future interest rates and relies on generous assumptions regarding future deficits and tax‑revenue growth. Yet the situation could deteriorate much further. Consider the impact if:

Prime Minister Takaichi increases the fiscal deficit, particularly through tax reductions;

Economic growth slows, simultaneously raising the deficit and reducing tax receipts;

The BoJ further reduces its balance sheet, amplifying upward pressure on yields.

Any combination of these risks would accelerate the deterioration in debt sustainability and push Japan toward a far more destabilising fiscal trajectory.

WHY COULD THIS BOIL OVER IN 2026?

Like many governments around the world, the Japanese could easily increase their deficit to boost growth and improve voter popularity . The BOJ has recently reiterated its stance on the Japanese fiscal situation, saying that it is for the government to sort. The BOJ is also saying that it cannot intervene in the JGB market as inflation is too high – perhaps to keep confidence in the Yen and Nikkei.

But the JGB government bond market and YEN are already both reacting in a negative way – yields are rising and the compression of global yields to Japanese yields has NOT brought about a strengthening of the Yen. More financial participants are beginning to realise that Japanese debt is no longer on a sustainable path with rising interest rates. A JGB and Yen crisis seems imminent.

Like many governments globally, Japan could choose to widen its fiscal deficit to support growth and bolster political support. The BoJ has recently reiterated its view that fiscal sustainability is the government’s responsibility and has argued that it cannot intervene in the JGB market while inflation remains elevated—possibly to maintain confidence in the Yen and the Nikkei.

However, both the JGB market and the Yen are already signalling stress. Yields continue to rise, and the narrowing of global yield differentials has not led to Yen appreciation.

Increasingly, market participants recognise that Japan’s debt trajectory is no longer sustainable in an environment of rising interest rates. A disorderly adjustment in both JGBs and the yen appears increasingly likely.

CONCLUSION

As yields continue to rise, the risk increases that investors begin to question the sustainability of Japan’s public finances. Higher interest rates would push debt‑servicing costs even further upward, driving the Interest Cost to Tax Revenue ratio into objectively dangerous territory. Such a trend would heighten instability across Japanese financial markets and increase the likelihood of volatility in both bonds and the currency.

Ultimately, it remains likely that when pressure becomes acute, the BoJ will reverse course and reintroduce large‑scale QQE or YCC, using its balance sheet to cap yields at levels it judges compatible with fiscal stability. A significant currency depreciation would then become the primary release valve for Japan’s excessive debt burden.

This currency debasement pattern has repeated throughout monetary history and would represent a return to the "Abenomics" framework, in contrast to the debt‑deflation dynamics that characterised the earlier "Lost Generation".

---------------------------------------------------------------------------------------------------------------------------

(*1) Some governments that run overall deficits still report primary surpluses, which exclude interest payments. However, once interest costs push these governments into a full deficit, they must still issue new debt both to cover those interest expenses and to refinance maturing bonds.

Comments